The original article is published on the IFRC website.

The world is facing record levels of people forced to flee their homes due to violence, insecurity, and the effects of climate change (UNHCR 2021). Many cannot return home and face the new overwhelming reality to resettle and rebuild somewhere from zero. As is the case for many protracted crises, how do we face the challenge of responding to the urgent needs while also the long-term solutions to help improve lives for the years to come?

By Deniz Kacmaz, IFRC Turkey, Livelihood Officer

Turkey is hosting the largest refugee population in the world. More than 3.7 million Syrians have sought refuge as well as 330,000 under international protection and those seeking asylum, including Iraqis, Afghans, Iranians, Somalis, among others. With the conflict in Syria now entering its twelfth year with few signs of change, means that we are not just looking at a humanitarian emergency anymore, but on long-term resilience.

Since the refugee influx began in Turkey, the Turkish Red Crescent (Türk Kızılay) has been taking a leading role in the response. As of April 2020, Turkish Red Crescent through its KIZILAYKART platform and IFRC run the largest humanitarian cash programme in the world, the Emergency Social Safety Net (ESSN), funded by the EU.

This programme has helped more than 1.5 million cover some of their most basic needs, covering their groceries, rent and utilities, medicine and their children’s school supplies.

But humanitarian emergency cash assistance can only go so far. There is also a need to focus on longer-term resilience. This is why we are working on both the urgent needs of refugees, while also supporting longer-term livelihood opportunities for refugees and host communities.

Photo: IFRC

From humanitarian cash to longer-term resilience

We are working on both the urgent needs of refugees, while also supporting longer-term livelihood opportunities for refugees and host communities. This means being part of the labour market to meet their own needs and rebuild their life without depending on social assistance, including the ESSN.

We must focus on long-term solutions where refugees, supported by the ESSN, gain their power to stand on their feet and become self-reliant again.

I have been working at IFRC Turkey Delegation for almost two years helping identify gaps and find opportunities to empower people’s socio-economic capacities. This approach helps ensure they are resilient in combating challenges in the future, including the devastating socio-economic impacts brought on by the COVID-19 pandemic and general obstacles around employment opportunities.

We have seen in many contexts when refugees are able to build their resilience and self-sufficiency, they can contribute even more meaningfully to the local economy. When they benefit, we all benefit, including host communities.

What are we doing to bring this long-term solution to the lives of refugees?

As of April 2021, we have launched referrals that link people receiving cash assistance through ESSN with a plethora of livelihood trainings and opportunities in Turkish Red Crescent community centres.

The 19 community centres across Turkey offer support to both refugee and host communities, including work permit support, vocational courses such as sewing; mask producing; various agricultural trainings; and Turkish language courses and skills trainings. These services are critical to breaking barriers in the local markets. The community centres connect skilled individuals to relevant job opportunities by coordinating with public institutions and other livelihood sector representatives.

The ESSN cash assistance provides support to refugees in the short term while giving them opportunities to learn new skills, which can lead to income generation in the long term.

How do we conduct referrals from the ESSN to livelihoods?

There are many sources where families are identified for referrals, some of the most common are:

- Turkish Red Crescent (Türk Kızılay) Service Centre

- 168 Kızılay Call Centre

- Direct e-mail address to the TRC referral and outreach team

- Identified potential individuals among ESSN protection cases

- Field teams including monitoring and evaluation and referral and outreach teams who are regularly engaging with those benefitting from ESSN

In the first months of combining cash assistance with longer-term programmes, we have supported more than 1,000 refugees.

Some have been referred to employment supports including consultancy for employment and work permit support, while others are attending language courses, vocational trainings, and skills development courses through public institutions, NGOs, UN agencies and TRC’s community centres.

Though we have developed a robust livelihood referral system, collectively, we need to make stronger investments in social economic empowerment in the future.

While we continue to work on improving our programming and referral mechanisms, as IFRC, we are also reaching out to agencies, civil society, donors, and authorities to look at how we can:

- increase investment in socio-economic empowerment in Turkey,

- mitigate barriers to employment for refugees, and

- create greater synergies between humanitarian and development interventions.

It is this collective effort that will deliver the longer-term gains necessary for both refugee and local communities in Turkey to thrive.

—

The ESSN is the largest humanitarian cash assistance program in the world, and it is funded by the European Union. The ESSN has been implemented nationwide in Turkey in coordination and collaboration with the Turkish Red Crescent and International Federation of Red Cross and Crescent Societies (IFRC). We reach more than 1.5 million refugees in Turkey through the ESSN, and we give cash assistance to the most vulnerable populations to make sure they meet their basic needs and live a dignified life.

The Turkish Red Crescent with its 19 community centres throughout Turkey supports millions of refugees as well as host communities. The Centres provide several courses, vocational trainings, social cohesion activities, health, psychosocial support, and protection services, among others.

This blog series will focus on the highlights from different Cash Practitioner Development Programme deployments in 2021, allowing practitioners to share what they have learnt and experienced during their Cash School learning deployments.

The Cash Practitioner Development Programme aims to expand the ready pool of cash experts available to deliver humanitarian cash assistance, and to strengthen the community of qualified practitioners with up-to-date skills in all areas of cash assistance. Cash deployments are a key element of participants learning schedules, these deployments aim to enhance skills and confidence in implementing cash based assistance. Some deployments are run in partnership with NORCAP, with practitioners accessing deployment opportunities from a range of humanitarian agencies.

Name : Danièle Wyss

Job title : Cash & Market Specialist – ICRC

Where were you deployed : Deployed to work with the Turkish Red Crescent (Ankara & Gaziantep)

What type of work did you complete as part of the deployment?

During the deployment I worked with the TRC’s Coordination and Project Coordination teams, the deployment aimed to provide experience in strategic CVA coordination, including the ESSN taskforces and coordination mechanisms under the Regional Refugee and Resilience Plan (3RP). I participated in their Basic Needs and CBI Working Group meetings.

I wrote a comprehensive paper on what is KizilayKart, how it works and what makes it such a success. It contains background information on the crisis, the Turkish Red Crescent, the registration process, the current and completed programes, the seven KizilayKart workflows/units, the internal and external coordination mechanisms, links to relevant websites, platforms etc and an ‘interview’ section resulting from my field trip to Gaziantep and Ankara where I was able to ask many questions about the process as a whole.

What have you learned most about?

My key learnings were:

- Good coordination between humanitarian actors and all stakeholder is possible

- Unless there is political will, no matter how much inter-agency coordination and how good it is, the response will not be a success

- AAP/CEA is essential for beneficiaries and non-beneficiaries alike but also for host-communities, staff and volunteers

- For such a response to be successful and to avoid unnecessary tension, the host community must be included in the process and the assistance

What was a ‘stand out’ moment for you on your deployment`?

For me it was definitely the field trip to Gaziantep where I was able to witness first hand all the work done by the TRC. We had the opportunity to speak with various departments from the Gaziantep ESSN office, visit a Community Centre and a Service Centre. We were able to interview numerous people, such as:

-> M&E field team

-> M&E Operators team

-> Call Centre team

-> Outreach team

-> In-camp Management team

-> Deputy coordinator

-> Community Centre team

-> Service Centre manager

It is quite impressive to see everyone’s dedication but also the variety of different nationalities working on the projects. A substential number of colleagues have been involved from the start of the crisis and worked in various departments/workstreams of the TRC and the KizilayKart project. Quite a few have themselves gone through the whole process, which means that they have a deep understanding and knowledge of all the programmes and know how to best address people’s queries and/or worries.

Author: Maja Tønning, Regional CVA Coordinator, IFRC Africa

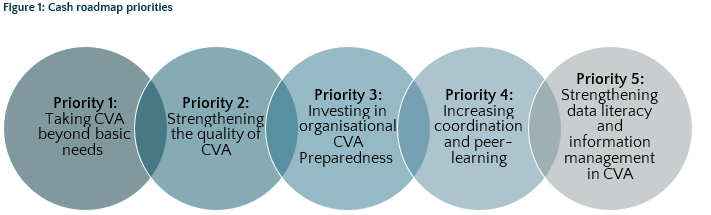

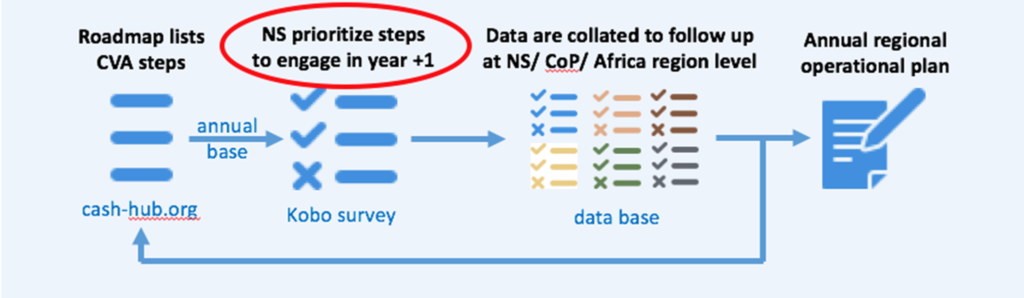

The IFRC in the Africa Region has coordinated the launch of an online Cash Community of Practice (CoP) for all African National Societies (ANS), now live on the Cash Hub platform. The online CoP seeks to connect all ANS and their partners and to strengthen peer learning and sharing. This online cash CoP will also host the Africa Cash Roadmap 2022-25 which is structured around National Society priorities and ongoing efforts and experiences in Cash and Voucher Assistance (CVA).

The Cash Roadmap and the online Cash CoP were based on consultations with 72% of African National Societies as well as the engagement of regional and global IFRC staff and partners, including ICRC, supporting CVA in Africa. In total, around 500 answers to challenges and opportunities were collected.

Great initiative, and really impressive to hear how many African NS have been involved in defining the needs.

PNS representative during the review session

The Africa Cash Roadmap consists of several related and integrated parts:

- A PDF which is an overall introduction to the Cash Roadmap and a narrative to use with partners, for fundraising and for external communication.

- The online Cash Community of Practice (CoP) for African National Societies, which can be accessed clicking on this link.

- The online Cash Roadmap outlining National Society priorities for CVA on an annual basis. Click here to access a web page dedicated to the Africa Cash Roadmap.

- An online Kobo survey, which feeds into the online Cash roadmap and specific action plans for National Societies in Africa.

Jordane Hesse who worked as a consultant on developing the Africa Cash Roadmap stated:

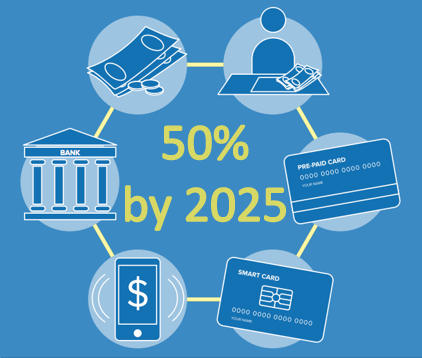

When the Movement established a CVA objective at 50% by 2025*, with 49 National Societies and many Partner National Societies having different starting points and challenges, an interactive roadmap became a must to support each ANS in scaling CVA, targeting qualitative and efficient interventions. The tool developed is a response to what the field voiced. It aims to support, facilitate, inspire each one of them, and will evolve over the next 4 years.

*the assistance delivered directly to households, i.e. between in-kind and CVA, excluding services

The online Cash CoP will be updated on a continuous basis and French translations will be available in early 2022. If any National Society or Partner has specific updates to share on CVA for the Africa Region, feel free to reach out to Maja.Tonning@ifrc.org and we can post these on the online Cash CoP as well.

Click here to read the original article published on the ICRC website.

The Analysis & Evidence Week 2021 – Data, data, data… but then what? provides a unique forum to engage in the common topics facing evidence-based decision-making in humanitarian action.

The event aims at bringing together humanitarian actors, the private sector, academia and beyond to discuss opportunities and challenges of data policies, methodologies and usage, while ensuring the analytical work is actionable and practices remain people-centred.

More than 2,000 people showed interest and participated to the event. Among them there were representatives of the Red Cross and Red Crescent Movement, UN agencies, NGOs, private sector, donor community and academia. On average 65 people attended each session with a peak of nearly 250 attendees at the Opening Ceremony.

If you were not able to attend some sessions, or you would like to listen in once more to the great initiatives and discussions broadcasted last week, you can find below the recordings to the 60+ sessions held during the event. The videos will be available online for 30 days, and can be downloaded for future reference.

Should you wish to have further information on the event and/or follow up on possible collaboration opportunities, do not hesitate to reach out to me and the rest of the A&E Team via email at EcoSecAnalysis@icrc.org

SESSION RECORDINGS

29 November 2021

- Opening Ceremony – ICRC

- Launch of the Needs Assessment and Targeting Guidelines – ICRC A&E

- Documenting and measuring the impact of attacks on healthcare: lessons learnt from Afghanistan – U. Geneva

- Seed Tracking Initiative in the Central African Republic – ICRC Central African Republic

- COVID-19 GO Dashboard a Federation-wide Data Collection Effort – IFRC

- Protection of Civilians: Criteria and Prioritization – ICRC Protection (internal session)

- Data Disaggregation: Just a reporting requirement, more data than we can handle, or an essential tool to leave no one behind? – ICRC AAP (internal session)

- Using data to inform decision-making for sustainable humanitarian logistics – U. Coventry / ICRC Logistics

- Monitoring operational resilience of essential service delivery in protracted urban armed conflicts – ICRC WatHab (No recording available, apologies for the inconvenience)

- JIAF: A Concept, Framework and Process for a Person-Centered Intersectoral Analysis – UN OCHA / ECHO

- Everything in space and time: Spatial analysis for humanitarian decision-support – HHI / Esri

- Analyzing Health and Conflict Data to Understand the Impact of IHL Violations – Berkeley U. / John Hopkins U. / LSHTM

01 December 2021

- Blurred Boundaries: Aspects & Challenges to Accountability in Operational Research – ICRC CORE

- Strengths in number, rethinking analytical capacities and network in the humanitarian sector – The Operation Partnership

- Informing Geographic Targeting with Secondary Data – ICRC Near and Middle East

- Overview of the Information Management Resource Portal – CartONG

- Data and Response to the Dangers Posed by Mines and Explosive Remnants of War – ICRC Weapon Contamination

- Protection Analytical Framework: A Common and Structured approach – DRC / IRC

- Emergency Assessment for a Joint Response to Mt. Nyiragongo Eruption in DRC – IFRC / Swedish RC

- Analysis & Evidence Opportunities and Career Paths in the ICRC – ICRC Talent Management

- Better Data, Better Decisions? – Will improved data sharing lead to improved decision-making in humanitarian response? – UN OCHA / WFP

- Strengths in Numbers: Rethinking Analytical Capacities and Networks in the Sector – The Operations Partnership

- COVID-19 GO Dashboard: a Federation-wide Data Collection Effort – IFRC

02 December 2021

- EpiWatch – Preventing the Next Pandemic – U. New South Wales

- Introducing the MEI Multiform – ICRC EcoSec (internal session)

- Remote Data Collection in Action (Bangladesh, Somalia) – ICRC Somalia and Myanmar

- Access to Basic Amenities at Household Level for Advocacy and Decision Making – MSF (Session cancelled due to no-show of speakers)

- Applying the INFORM Quantitative Analysis for Humanitarian Aid Decision-Making – ECHO

- Learning from Disruption: from Covid-19 Monitoring to Situation Monitoring – ICRC A&E

- Addressing Climate Change through Participatory Mapping in Rural Tajikistan – CartONG

- Diving into DEEP: Promoting a Collaborative Approach to Humanitarian Analysis – DRC

- Water & Habitat – Enhancing the Planning, Monitoring and Evaluation Cycle – ICRC WatHab (internal session)

- Bridging the Gap between Global and Regional: A connected Impactful Analysis – ACAPS

- Multidisciplinary Assessments: Lessons Learnt from the Middle East – JIPS / ICRC Near and Middle East

- Evidence-Based Practice to Support Humanitarian and Development Aid Activities – Belgian RC

- Opportunities and challenges of Data Policies, Methods and usage in the private sector – U. Muni (Session cancelled due to no-show of speakers)

- Using web surveys to Inform Decision Making in Latin America – WFP

- Blurred Boundaries: Aspects and Challenges to Accountability in Operational Research – ICRC CORE

- Crowdsourcing Data for Real-time Insights – Premise

- Community-Based Surveillance and Nyss in Somaliland – Norwegian RC

03 December 2021

- Nutrition Outcome Analysis – Independent Speaker

- Remote Sensing and Spatial Analysis to Complement Field Work – ICRC GIS

- How Much Data is Enough Data? Drivers of Over-Collection and Red Lines – GPPi

- Accessibility to Toilets and Inclusion: Lessons from Indonesia – ICRC Indonesia

- Data Protection in Action – FAQs for Assistance Programmes – ICRC Data Protection Office

- The UK Hardship Fund – Financial Support for the Most Vulnerable during COVID-19 – British RC

- Needs Assessments and Data Management in Fragile Contexts – PwC

- Remote Management of Affected People – ICRC A&E

- Getting to Impact: Right-Sizing Evidence Collection in Humanitarian Crisis – Salesforce

- The Framework for the Ethical Assessment of Humanitarian Drones – U. Geneva / U. Zurich

- Accountability to Whom? – ICRC Data Protection Office

- Emergency Assessment for a Joint Response to Mt. Nyiragongo Eruption in DRC – IFRC

- The effect of UN Peacekeeping Stabilization Projects on Humanitarian Access – European Institute U.

- How Much Data is Enough Data? Drivers of Over-Collection and Red Lines – GPPi

- Evaluating a Digital Innovation: an Overview of CommCare’s Evidence Base – Dimagi

- Closing Ceremony – ICRC

This blog series will focus on the highlights from different Cash Practitioner Development Programme deployments in 2021, allowing practitioners to share what they have learnt and experienced during their Cash School learning deployments.

The Cash Practitioner Development Programme aims to expand the ready pool of cash experts available to deliver humanitarian cash assistance, and to strengthen the community of qualified practitioners with up-to-date skills in all areas of cash assistance. Cash deployments are a key element of participants learning schedules, these deployments aim to enhance skills and confidence in implementing cash based assistance. Some deployments are run in partnership with NORCAP, with practitioners accessing deployment opportunities from a range of humanitarian agencies.

Name: Shubhadra Devkota

Job Title: Senior Programme and Livelihood Officer, DRC Country Office Nepal

Where were you deployed?

Remotely deployed to the Africa Region to work with Ghana Red Cross Society (GRCS), Nigeria Red Cross Society (NRCS), and Rwanda Red Cross Society (RRCS).

What type of CVA work did you complete as part of the deployment?

I supported the development of the Cash and Voucher Assistance (CVA) Generic Risk Register and user guidelines which shall be used by National Societies (NSs) in the Africa region. While developing this template I ensured coordination with the CVA risk advisor and the protection gender and inclusion advisor of the Africa region, as well as with the information management and data protection advisor from Geneva to capture the context of the region and include risks related to all sectors.

The active involvement and contribution from the CVA teams of three different NSs (GRCS, RRCS and NRCS ) was outstanding. Alongside consultations with sectoral experts and working sessions with CVA teams, a desk review and analysis of available reference materials was conducted from different sources to develop the CVA risk register. I also conducted a series of briefing and working sessions on CVA risk analysis and on the CVA risk register, as well as a short briefing session with the Zambia Red Cross team.

What was the area you learnt most about?

- Development of CVA risk register & user guideline

- CVA risk analysis skills for NSs

- How to use information from the CVA risk register to inform response analysis and CVA programme design

- Virtual working sessions, briefings, and trainings working collaboratively with NSs

- Africa Region Cash Coordination structure

What was a ‘stand out’ moment for you on your deployment?

Preparing a ‘ready to use’ generic CVA risk register and user guidelines acceptable to the region, in consultation with sectoral experts. I also enjoyed the active engagement of different NSs of the region which I consider a “stand out” moment for me during this deployment. Coordination with multiple experts, multiple NSs and managing time in their busy schedules was not an easy task. However, with the teams’ support and input, the CVA risk register and user guidelines were ready within six weeks of my deployment period.

I was also able to share the tools during an online learning session on “Risk management in CVA and the CVA-risk matrix” for NSs, partner NSs and IFRC representatives of the region. The suggestions and reflections from the wide range of participants was another “stand out” moment for me, which indicated that tools shall be used in other contexts and not only in the Africa region.

This blog series will focus on the highlights from different Cash Practitioner Development Programme deployments in 2021, allowing practitioners to share what they have learnt and experienced during their Cash School learning deployments.

The Cash Practitioner Development Programme aims to expand the ready pool of cash experts available to deliver humanitarian cash assistance, and to strengthen the community of qualified practitioners with up-to-date skills in all areas of cash assistance. Cash deployments are a key element of participants learning schedules, these deployments aim to enhance skills and confidence in implementing cash based assistance. Some deployments are run in partnership with NORCAP, with practitioners accessing deployment opportunities from a range of humanitarian agencies.

Name: Ali Eren Karadeniz

Job Title: Cash and Voucher Assistance Officer, Turkish Red Crescent

Where were you deployed?

Remotely deployed to work with Indonesia Cash Working Group

What type of CVA work did you complete as part of the deployment?

During the deployment, I have supported the Indonesia Cash Working Group (CWG) to develop Minimum Expenditure Basket (MEB). In order to facilitate the MEB development process for the CWG, I worked on creating a framework document which the CWG benefitted to shape the discussions on how to calculate the MEB in the best way possible as per their operational needs. This required an intense secondary data review and analysis as well as timely and swift coordination with all members within the CWG.

What was the area you learnt most about?

The areas I learnt most about and grew my skills in were:

- Asia-Pacific region cash coordination structure,

- Overall MEB development process and examples around the world,

- Facilitating decision making in a complex humanitarian environment,

- Remote coordination with humanitarian actors.

What was a ‘stand out’ moment for you on your deployment?

Joining a cash working group for a specific task and for a limited time frame has its own challenges such as developing a mutual understanding between multiple partners and working in close collaboration in a systemized and coordinated way. It was a great feeling when all CWG members agreed upon the geographical scope of the MEB after several discussions and I was quite happy that I could contribute to CWG’s decision making process in a positive way.

Another moment that stood out for me during the deployment was when we, as the CWG, have engaged with the broader humanitarian scheme in Indonesia for their contributions on the MEB. Collecting inputs from different clusters including health, shelter, education etc. have helped the CWG to understand the needs better and make informed decisions about which food and non-food items must be kept within the MEB, which would serve as a baseline for future discussions around assistance amount.

Author: IFRC Cash team

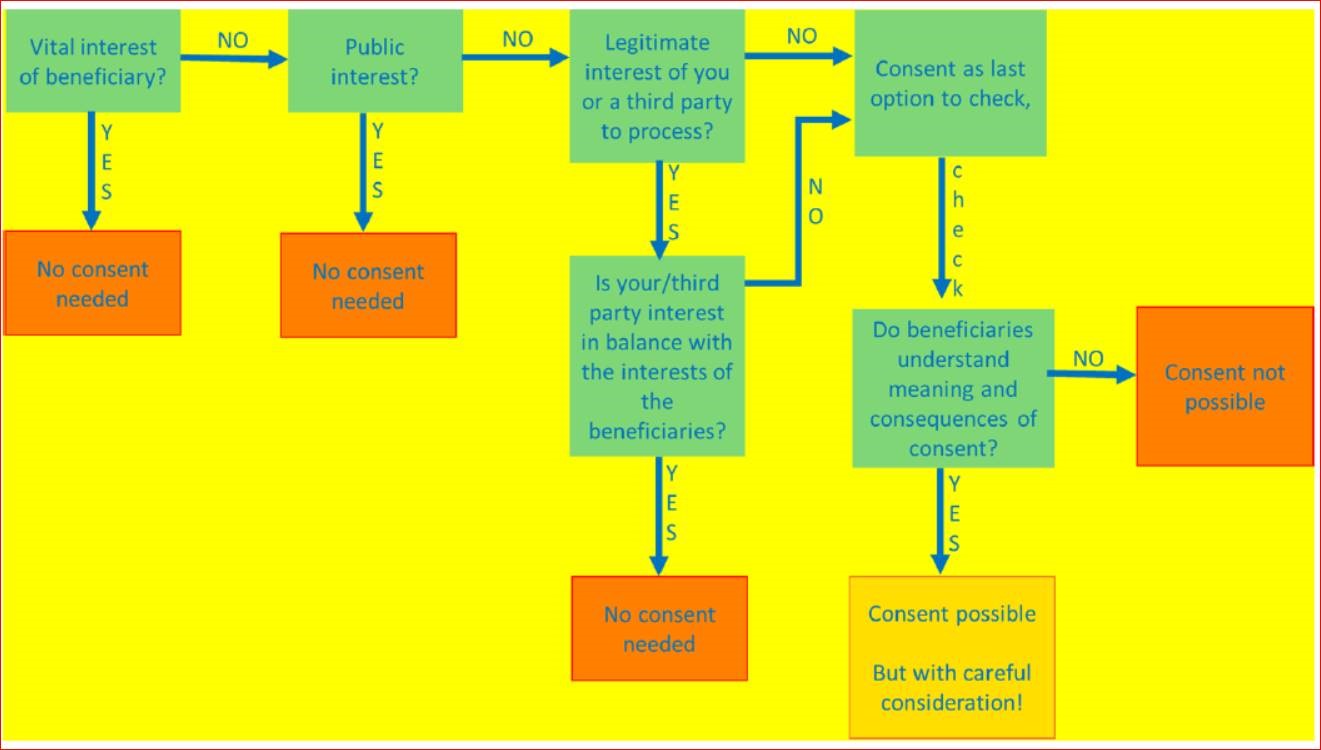

The IFRC has published a practical guidance on Data Protection and Cash and Voucher Assistance (CVA) to help staff and volunteers apply data protection principles in their delivery of humanitarian cash and voucher. The guidance, which complements the Cash in Emergencies Toolkit, lays out the key principles of data protection and carefully guides the reader through the processes of CVA from targeting to post-distribution monitoring, asking a set of critical questions at each stage. Many of the questions are also illustrated by examples and practical advice on how to apply the guidance. The questions include, for example:

- What legitimate basis should I rely on and is consent the most appropriate?

- Do I absolutely need the data collected by an external source and how can I make sure the beneficiary data has been collected in an appropriate manner?

- Is it necessary and safe to share personal data with the donors?

By formulating key questions in an accurate way, the guidance gives practitioners a practical framework for taking decisions in the best interest of the communities they serve.

According to the guidance:

“Data protection is not only a matter of good governance; it is also about building trust.”

Beneficiary trust is, of course, vital for CVA and other humanitarian programmes to succeed. Therefore, by embedding data protection principles into programmes from the outset, practitioners are not only attending to beneficiaries, but also enhancing the reputation of their organisations.

in Cash and Voucher Assistance )

To find out more about this document, watch the recording of this webinar organised to launch the new Practical Guidance for Data Protection in Cash and Voucher Assistance – A supplement to the Cash in Emergencies Toolkit:

Practical Guidance for Data Protection in Cash and Voucher Assistance – A supplement to the Cash in Emergencies Toolkit from Cash Hub on Vimeo.

Find out more:

- Link to CVA Data Protection Guidance: https://cash-hub.org/resource/practical-guidance-for-data-protection-in-cash-and-voucher-assistance-a-supplement-to-the-cash-in-emergencies-toolkit/

- Link to the Cash Hub’s webinar on Cash and Data Protection: https://cash-hub.org/resources/webinar-series/#webinar-18

- Link to webinar introducing the CVA Data Protection guidance: https://cash-hub.org/resource/practical-guidance-for-data-protection-in-cash-and-voucher-assistance-a-supplement-to-the-cash-in-emergencies-toolkit-2/

- Link to CaLP’s webinar: Data simplified. Protection amplified. An essential conversation for CVA practitioners: https://www.youtube.com/playlist?list=PLXAi0e320HJwhYFSwpqtL3O0yBPzj-YEU

- Link to ICRC video on Data Protection and Cash Transfer: https://www.youtube.com/watch?v=FfHVagVaK4w&feature=emb_logo

- Link to Digital Dilemmas Dialogue – A Humanitarian look at Assistance Programming and Social Protection Systems: https://www.icrc.org/en/digitharium/digital-dilemmas-dialogue-2

This blog series will focus on the highlights from different Cash Practitioner Development Programme deployments in 2021, allowing practitioners to share what they have learnt and experienced during their Cash School learning deployments.

The Cash Practitioner Development Programme aims to expand the ready pool of cash experts available to deliver humanitarian cash assistance, and to strengthen the community of qualified practitioners with up-to-date skills in all areas of cash assistance. Over the course of one year, participants learning schedules are tailored to their needs and personal experience to date. Cash deployments are a key element of participants learning schedules, these deployments aim to enhance skills and confidence in implementing cash based assistance. Some deployments are run in partnership with NORCAP, with practitioners accessing deployment opportunities from a range of humanitarian agencies. Practitioners can expect to learn experientially through work activities, and to review and evaluate their learning after every deployment.

Name: Nabeh Allaham

Job Title: Cash and Voucher Assistance Coordinator, Syrian Arab Red Crescent (SARC)

Where were you deployed?

South Sudan, Juba, into the role of Cash Working Group (CWG) co-lead.

What type of CVA work did you complete as part of the deployment?

During this deployment the role of the CWG co-lead in Juba covered a range of tasks, these included: reviewing key documents (Survival Minimum Expenditure Basket, CWG South Sudan Terms of Reference, Cash for Work Guidelines, and South Sudan Humanitarian Fund proposals); supporting the Financial Service Providers, partners and National Society to understand what their main challenges are in the area of CVA; and working on Financial Service Provider mapping.

What was the area you learnt most about?

The areas I learnt most about and grew my skills in were:

- Modalities and Delivery Mechanisms selection

- Partnerships , coordination network

- Development of CVA Terms of Reference

- Cash for Work technical knowledge

- Strategic Directions setting for CWG

- Calculation process of S/MEB.

What was a ‘stand out’ moment for you on your deployment?

There were many key moments from this deployment which stood out. One was the opportunity to be more involved in working with the CWG, getting a better idea about the way in which CWGs work, what are the most important factors that should be considered while supporting and building the capacity of a national and international organization, and understanding the role that CWGs can play in enhancing the coordination and harmonization of the national and international CVA levels.

Other key moments have been: gaining an extensive knowledge of the UN environment system and how much it is different to a National Society; learning that best and important skills that a CWG coordinator should have are being able to keep the network between all the humanitarian actors stable and effective; experiencing how to deal and participate in a new, complicated and complex context with all the stockholders; and learning the role that I have to play in supporting, convening and encouraging CVA parties to participate and help in taking the decisions.

In 2020, the outbreak of COVID-19 in the UK prevented many people from accessing their usual forms of financial support and drove many more into unemployment and severe financial hardship. In line with its mandate, the British Red Cross responded by launching a new emergency cash service: the UK Hardship Fund. The Fund was made possible thanks to a generous donation from a British Red Cross’ partner, Aviva and the Aviva Foundation, with the aim of providing nation-wide, short-term financial assistance to people who are struggling to meet their essential needs.

The Fund offered a tool for British Red Cross and their partner charities to deliver short term direct cash assistance to people, all run through a centralised system at the British Red Cross. Designed for people with complex needs and no income, the Fund offered a one-off payment of £120 or a three-month grant of £360 paid in monthly instalments. As of April 2021, the British Red Cross has distributed £3.1 million in cash grants, supporting 13,016 people.

When you hear feedback, it is easy to appreciate what a difference £120 can make to someone’s life […]. When you have nothing, no income or other form or assistance, this support can make the difference between whether you eat or not in a given day; the fund targets the most vulnerable people who are unable to access any other form of support.

Alex Ballard

Alex Ballard, the Hardship Fund Programme Manager, has offered his thoughts on the most important components of the Hardship Fund: the role of partnerships and the use of technology.

How have partnerships helped the British Red Cross to reach the most vulnerable?

One of the first tasks for the Hardship Fund team was to identify those who most urgently needed financial support: those for whom this Fund represented their only option to meet their needs. This led the team to establish an eligibility criteria that encompassed a no income threshold as well as certain indicators of vulnerability, such as an unstable migration status, deterioration in physical or mental health, or risk of domestic violence. To ensure that they could identify those who met this criteria across the UK, the British Red Cross turned to external organisations who were already working with many of these groups, creating a network of over 300 referral partners.

Thanks to this network of partners, the Fund was able to reach a larger and broader range of people, reflecting the complex and wide-ranging impact of COVID-19 on financial resilience. The aim of the partnership approach was two-fold: to expand the reach of this Fund, and also to ensure that this short-term cash assistance did not stand on its own, and instead complemented longer-term solutions and casework relationships through these engaged partners.

In engaging with partners, the British Red Cross adopted a national approach through regional teams, who were able to build on their local knowledge and existing networks, as well as develop new, exciting partnerships and connections. Alex explains: “we relied on our regional approach to tap into existing local knowledge, which we were able to do well thanks to the long-term presence of BRC teams and the trust that has been built up through volunteers over many years.

The Hardship Fund team showing Bankable Visa cards that will be distributed to deliver cash assistance

By connecting with new partners – local authorities, charities, food banks and community groups – this impact was multiplied, as we were able to connect with wonderful groups deeply involved in their local communities. The long-term value comes from this community connection”.

For future cash programmes, Alex would recommend the partnership approach, but states it could not have been successful without significant time and effort invested into relationship management by regional Hardship Fund leads across the country, who work with partners to support the process and ensure the details of the Fund are explained accurately and uniformly across over 300 organisations.

To steer its vulnerability criteria and partnership approach, one tool used by the British Red Cross is its vulnerability index. This highlights which areas would be expected to have a greater concentration of people in need of support in the UK. The team used this to ensure they were working with organisations in the areas of greatest need, and to ensure a needs-led approach independent of geography.

Data management to scale up assistance during lockdown

Scaling up to safely distribute cash to over 10,000 people, through a process and team that had to work almost entirely remotely, was a unique challenge for the British Red Cross and required the use of secure and adaptable technology.

To do this, the Hardship Fund team collaborated with RedRose, who provided a ready-to-go data management system, and Bankable, who provided regulated cash cards. Thanks to a pre-existing service agreement between RedRose and the International Federation of the Red Cross and Red Crescent (IFRC), the RedRose system was able to be set up rapidly at the start of this response. Alex stresses how, while this technology is often used in less developed contexts, the Hardship Fund showed how RedRose can work everywhere.

Using this technology, the British Red Cross and partners would support somebody to undertake a criteria check and register for the Fund. On successful registration, this person would be sent a cash card, and use a mobile phone to verify with the Hardship Fund team, before cash is remotely uploaded onto the card. If verification is not accurate, an automated support system kicks in. In most cases, sending the card through the post is done on the same day of registration, and the card can be activated electronically, as soon as it has been received and verified. Alex raises the point that:

however clever your system is, there will always be somebody for whom this system doesn’t work. What about someone who doesn’t speak English so well or isn’t comfortable with using text messages? It is important to learn and improve continuously.

Alex Ballard

For this reason, the team established a helpline manned by dedicated staff, and a troubleshooting system. Insights from this and feedback from card users and partners led the team to start offering the instruction letter in 27 languages, to facilitate a smoother process and support a better user experience.

Working with RedRose offered new insights thanks to the data collection opportunities, enabling Information Management experts at the British Red Cross to create dashboards and analyse gaps and trends, steering the development of the programme. Alex explains that these data tools offer a smart overview of quantitative data, that can help us raise the right questions clarifying that these insights can help us challenge our expectations and ensure we are reaching the right people at the right time.

For the Hardship Fund team, the key question for improvement and evaluation has been whether the most vulnerable people have been reached.

We feel that we met the objective of helping even more people that we originally thought we would able to. Given our criteria, anyone we did support was effectively in extreme need of support.

Alex Ballard

Taking referrals from partners stops at the end of June 2021 and although the Hardship Fund will not be continued into the recovery phase, Alex feels that the learning it offers – particularly around about how to work with cash, how to use data and how to harness partnerships – could support stronger, integrated cash services in whatever comes next for cash assistance in the UK.

All feedback received has been incredibly positive and highlighted how the cash allowed people to choose the right assistance for their own needs. The stories we’ve heard from our incredible partners and service users are so inspiring and confirm the impact working together as a sector, using the right technology, and cash assistance can have to support people to prioritise and respond to their own needs at this difficult time.

Alex Ballard

The Baphalali Eswatini Red Cross Society (BERCS) and British Red Cross have published a new case study outlining how BERCS used their experience in cash and voucher assistance (CVA) to influence the Government of Eswatini to adopt mobile cash as the response modality for their humanitarian response and social protection programmes, since the COVID-19 response.

BERCS began advocating about the benefits of CVA in 2016 when they became the first actor in Eswatini to implement cash assistance. The advocacy work was essential to gain the government support needed to pilot a multipurpose cash programme, and throughout the programme transparent communication between BERCS and the government convinced many of the benefits and efficiencies of using CVA. This set a precedent and opened the path for other actors to implement CVA in Eswatini.

When the COVID-19 pandemic hit Eswatini in March 2020, the Government could not distribute goods in kind in the traditional way. Drawing on the advocacy and experience of BERCS and other actors, the Government implemented the first government funded response using mobile cash.

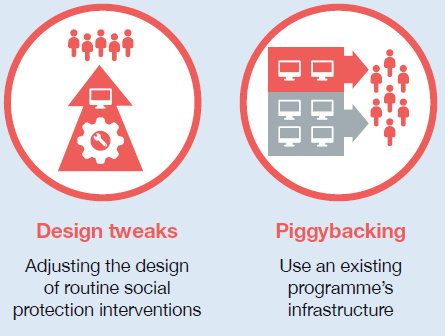

BERCS was actively consulted and used its experience to inform the response plan. The response was a success, covering 25% of the population with 91% of recipients confirming they were happy with the support.In line with this success, the Government of Eswatini also switched the modality of existing social assistance programmes from cash in envelopes to mobile money. This is known as a ‘tweak’ to the social protection system. This is a practical example of how BERCS’ advocacy efforts resulted in a more efficient and streamlined delivery mechanism for social assistance.

BERCS continues to work closely with the government and there are opportunities to further strengthen the links between humanitarian response and social assistance. Globally, National Societies are well-positioned to use their auxiliary role and expertise to advocate for wider use of CVA as one step to strengthen social protection systems, which can be adapted in different ways to better support those in need.

For more information about the experience in Eswatini and the unique role that National Societies can play to improve social protection mechanisms, download the full case study here.

The Cash and Social Protection page also offers access to many different resources explaining what social protection is and how National Societies can engage in this area.